McG

Army.ca Legend

- Reaction score

- 6,302

- Points

- 1,260

Here’s an idea to ponder.

And an interesting observation:

And an interesting observation:

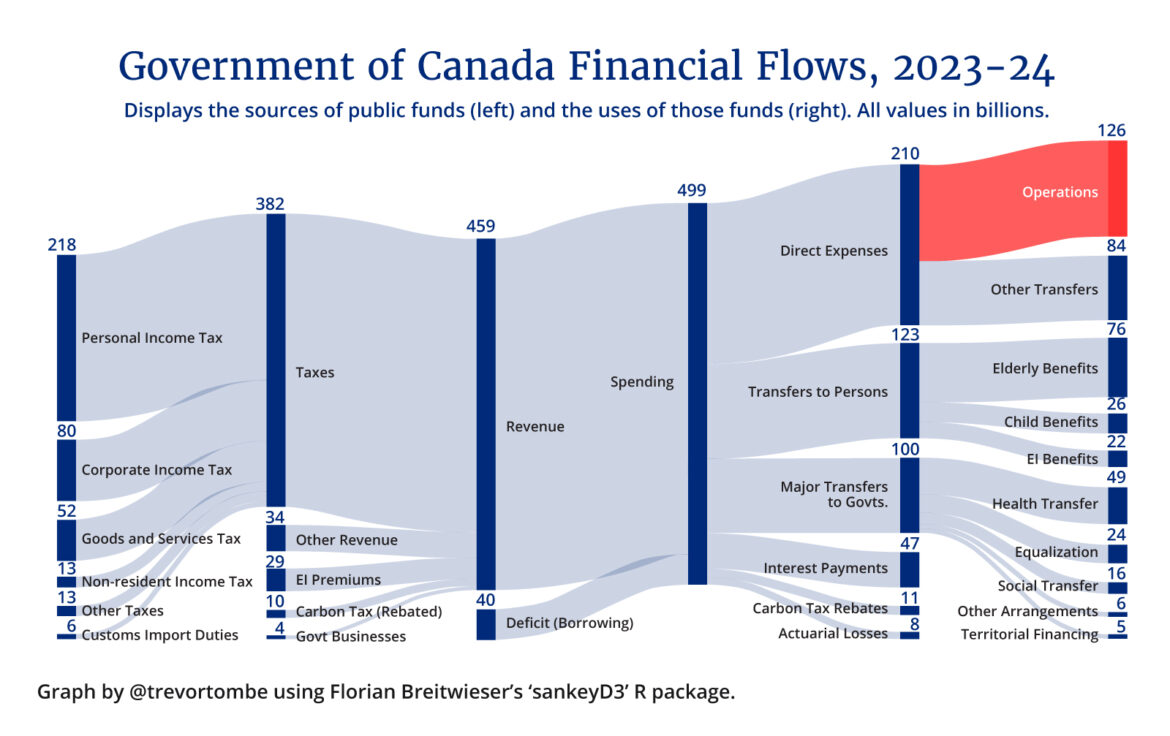

The trouble is, restraining direct federal expenses doesn’t get you very far.

In fact, you could fire every single federal employee (excluding the military and RCMP) and still come up short!1 You could defund the CBC, privatize Via Rail, eliminate any program with the word climate or energy efficiency in the title, close every single regional economic development agency, and disband the entire Department of Canadian Heritage, and the deficit would be cut by barely more than one-fifth.

I suspect a lot would come from Boomers. As a Gen-X’er left outside to play growing up while both parents were out working, I personally could deal with having no OAS at all, for example, since I foresee balancing my (reasonable I think) expectations with my earlier contributions. That said, I have little to no confidence that a socially-over focused government wouldn’t just blast those such ‘savings’ into oblivion like has developed over the last…checks calendar…8.173 years.

I suspect a lot would come from Boomers. As a Gen-X’er left outside to play growing up while both parents were out working, I personally could deal with having no OAS at all, for example, since I foresee balancing my (reasonable I think) expectations with my earlier contributions. That said, I have little to no confidence that a socially-over focused government wouldn’t just blast those such ‘savings’ into oblivion like has developed over the last…checks calendar…8.173 years.